Receipts: Social Security Does Not Add To The National Debt

There is plenty of confusion about how Social Security is budgeted and how its funds have been used in the past, which makes it a target for misinformation from those who want to eliminate or destroy the program.

The most common piece of misinformation is that Social Security adds to the national debt and, for that reason, the program must be cut or privatized.

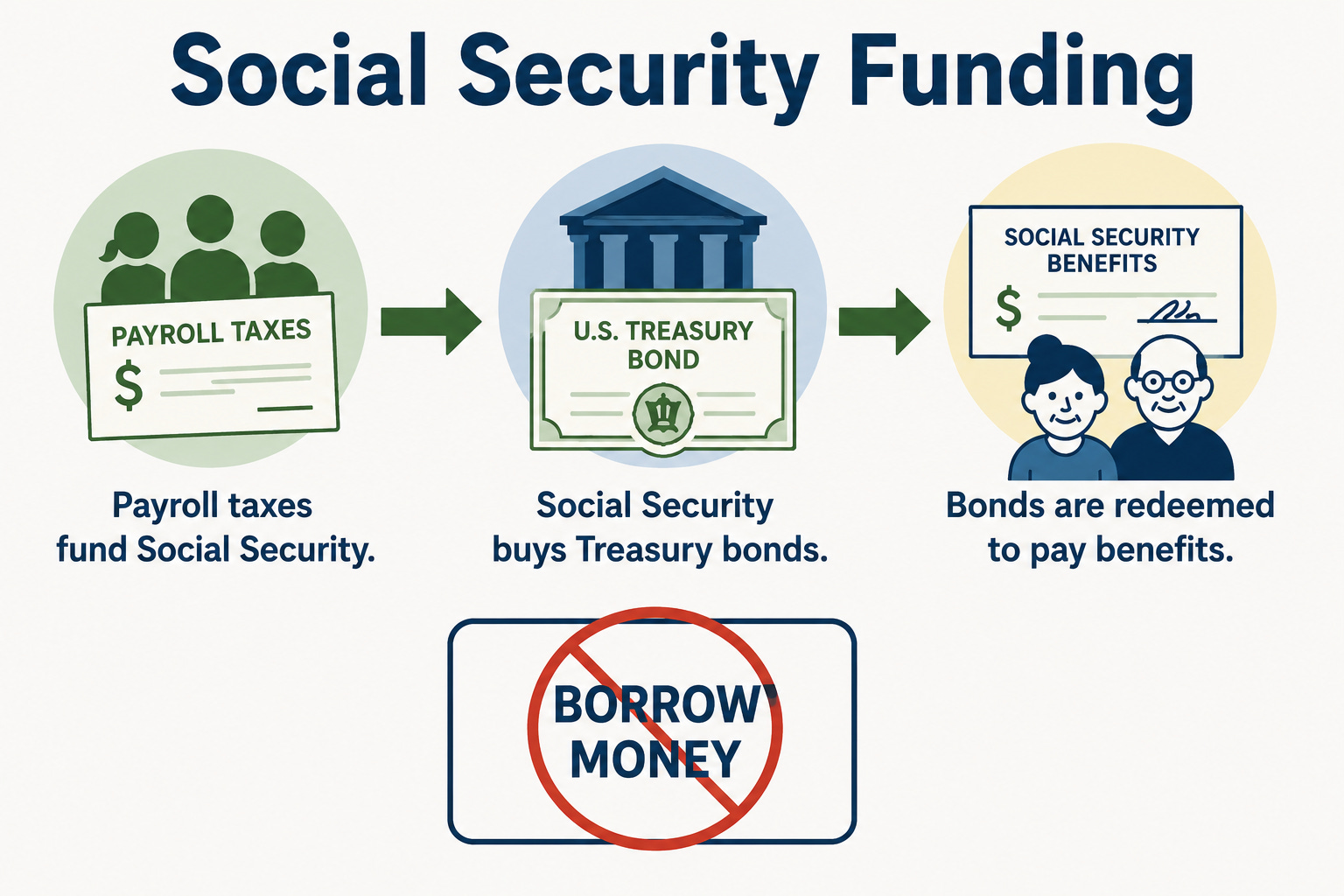

Social Security does not add to the debt. It has a shortfall, but that has nothing to do with the debt. It uses its trust fund built from past surpluses to cover the difference and is prohibited by law from borrowing money.

We will discuss each aspect of Social Security finances and how it all works.

How Social Security Budgeting Works

Social Security is funded mainly by payroll taxes, along with interest on its trust-fund securities and income taxes paid on some Social Security benefits. It is prohibited by law from borrowing money.

When Social Security has a surplus, it is required to invest those funds in Treasuries, including both special-issue Treasuries, which are available only to government trust funds such as Social Security, and publicly available Treasuries that you or I can also buy. These days, Social Security only holds special-issue Treasuries.

Bonds, which are what Treasuries are, are a standard way to raise money. They have three parts: the principal, maturity date, and interest rate. Purchasing a bond is giving a loan to the bond issuer, in this case, the federal government. There are also corporate bonds and municipal bonds, which are bonds issued by state and local governments. You purchase a bond at the principal value, and when the bond matures, the issuer of the bond pays you back the principal. During the duration of the bond, interest payments are paid to the holder at regular intervals. Special-issue Treasury securities differ from public Treasury securities because the trust funds can redeem them at face value when needed to pay benefits, rather than selling them on the open market.

An issuer of a bond agrees to take a loan to cover costs today, in exchange for paying interest on that loan until it is repaid in full at the end of the loan period. It is similar to a loan, such as a 30-year mortgage, where you agree to a repayment schedule and an interest rate. You have borrowed money to meet your needs and have an obligation to repay it with interest.

Because Social Security routinely buys bonds, there is a constant stream of bonds reaching their maturity date. When that happens, Social Security has two options. If the amount coming in from payroll taxes is sufficient to cover the program’s current expenses, the funds are reinvested in new bonds; this is called rolling over a bond. If the amount from payroll taxes isn’t sufficient, then the funds from the maturing bonds are applied to Social Security benefit payments.

In the past, Social Security amassed a sizable trust fund. Today, it is cashing out bonds far more often than it is investing new money. The reason is that people are living longer than in the past, and the boomer generation, named for the baby boom at that time, is especially large. In 1960, there were 5.1 people paying into Social Security for every beneficiary. Today, there are only 2.7.

Sources for this section

SSA — “Special-issue securities, Social Security trust funds” - Explains special-issue Treasury securities, public issues, certificates of indebtedness, long-term bonds, and why the trust funds now hold only special issues.

SSA — “Trust fund FAQs” - Explains that trust-fund income must be invested in federal securities and that special issues can be redeemed at face value when needed.

SSA — Social Security Act §201 - Legal basis for the OASI and DI trust funds, trust-fund investments, full faith and credit backing, and benefit payments from the trust funds.

SSA — “What are the Trust Funds?” - Plain-language explanation of what the trust funds are, what they can be used for, and how securities are redeemed.

SSA — “Fast Facts & Figures About Social Security, 2025” - Includes worker-to-beneficiary ratios, including 5.1 workers per beneficiary in 1960 and recent ratios.

The Basis Of The Claim That Social Security Adds To The National Debt

The entire basis of the claim that Social Security adds to the national debt revolves around these bonds and the current government budget. The federal government has had a deficit for the past 25 years. It was $1.8 trillion last year. Because the government is running a deficit, it has to borrow money to pay its debts, further increasing the national debt.

The claim is that when Social Security redeems Treasury securities to pay benefits, the Treasury may need to borrow from the public to get the cash, increasing publicly held debt. But by that logic, every person, institution, and country that owns a Treasury, such as a T-Bill or T-Note, is causing the debt to rise. The reality is that the government needs to borrow money to fund itself, someone has to hold that debt, and the government has a responsibility to repay those loans. The source of the new debt is the federal government’s unbalanced budget that doesn’t meet its obligations, not Social Security, you, or me, for loaning the government money by buying a Treasury note.

If you take out a car loan and, because you don’t have the money to make your obligated payments, you take out another loan to cover them, is the car or the car loan increasing your debt? Or was it from you making an obligation that you could not fulfill?

Social Security does not add to the national debt.

Sources for this section

Tax Policy Center — “Are the Social Security trust funds real?” - Explainer confirming the trust funds are real obligations while explaining the budget impact of redemption.

SSA — “The Social Security Trust Funds and the Federal Budget” - Explains unified budget treatment and the sense in which payroll tax surpluses invested in Treasury securities are lent to the federal government.

Is Social Security Running Out Of Money?

Another common statement is that in a decade or so, Social Security will run out of money and no one will receive benefits. That is not accurate.

Social Security has two trust funds: Old-Age and Survivors Insurance (OASI), which pays retirement benefits, and Disability Insurance (DI).

The Social Security OASI trust fund, funded by past surpluses, is being depleted and is expected to run out in less than a decade if nothing changes. But Social Security will continue to collect payroll taxes and pay out as much of the benefits as it can with that revenue. People will still receive benefits, but because Social Security is specifically prohibited from borrowing, benefits will decrease by about 25%.

This is still a serious problem because Social Security benefits are barely enough, and often too low, to serve the needs of recipients today. A significant reduction would cause substantial hardship for millions of Americans.

The DI trust fund is well-funded and will not be exhausted for several decades.

Sources for this section

SSA — “Trustees Report Summary” - Current trust-fund depletion projections and percent of benefits payable after depletion.

Did The Government “Raid” The Social Security Trust Fund?

No.

There is a lot of confusion around the Social Security Trust Fund and federal budgets, as well as about an authorized inter-Trust Fund borrowing in the 1980s. Let’s clear that up.

Today, the federal government looks at revenue and spending through a unified budget. That means taking all expenses and all incomes, combining them, and looking at the overall state of the finances. This does not mean that all money is put into a shared giant slush fund and used as needed. The trust funds are still legally separate. The unified budget is simply to make the budget easier to understand, although doing so blurs the difference between Social Security and the general fund, which creates the confusion we see today.

We often hear about publicly held debt vs government held debt. For example, there is around $32 trillion in publicly held debt compared to $39 trillion in overall debt, which includes intergovernmental debt.

Previously, we discussed how Social Security buys special-issue Treasuries rather than publicly traded bonds. This classifies the surplus held by Social Security as intergovernmental debt. This does not mean the government money is a single pool that can be used for whatever it wants. All programs and trust funds have their own accounting, and laws govern how money can be used.

The government cannot take money from the Social Security Trust Funds to pay for other things like the military, education, or interest on its debt, and Social Security is not allowed to borrow money from other government sources to cover its costs. They are separate; only reported together for ease of understanding.

There were two times in 1982 when very specific borrowing was undertaken among the OASI trust fund, the DI trust fund, and the Medicare Hospital Insurance trust fund to address short-term cash flow issues. In this case, around $17 billion was moved into the OASI, and that amount was fully repaid in 1986. The borrowing was permitted only by a law passed in 1981 for this purpose.

The federal government has never raided or borrowed from Social Security Trust Funds. Social Security Trust Funds use their surpluses to buy government debt through Treasuries, which is how the program is designed to work. The government hasn’t dipped its hands into the funds to siphon away your money.

Sources for this section

SSA — “Internet Myths Part 2” - Debunks the claim that Social Security was put into the general fund and explains the budget-accounting confusion.

SSA — “The Social Security Trust Funds and the Federal Budget” - Explains unified budget treatment and the sense in which payroll tax surpluses invested in Treasury securities are lent to the federal government.

SSA — “Inter-Fund Borrowing Among the Trust Funds” - Explains the early-1980s interfund borrowing among OASI, DI, and HI and repayment requirements.

How Do We Address The Shortfall

Social Security does have a shortfall and will exhaust its trust funds if the issue is not addressed. So how do we address it?

The first option is to reduce benefits, which will allow the trust funds to last longer. Since benefits are already too low, this option doesn’t properly address the issue.

The second option is to increase the retirement age, which will reduce the number of beneficiaries and lower the cost of the program. Not surprisingly, people who have been working for 40 years or more wouldn’t be happy to be told their retirement has been pushed back another five years. This is not a politically popular option.

The third option is to remove the cap on Social Security payroll taxes. The current cap is on earnings up to $184,500. Any income above that amount is not taxed for Social Security. Capital gains, money earned by selling investments such as stocks, aren’t taxed for Social Security at all. Increasing or removing the tax cap altogether would increase revenue to the program and add decades of runway to the trust funds. It is worth noting that the tax cap was removed from Medicare in 1993 specifically to ensure the program was better funded. And one last note: raising the tax cap does not mean that maximum benefits must be increased, which is an often-cited reason for not adjusting the cap. Medicare benefits were not increased when its tax cap was removed.

The fourth option is to implement means testing for benefits, which is a fancy way of saying that Social Security benefits would no longer be given to people with high incomes or significant wealth in retirement, leaving more money for those who genuinely need the benefits. Many federal programs, such as food, healthcare, and housing assistance, work this way.

The fifth option is to increase the population so that there is a better ratio of people paying into Social Security to those receiving benefits. America’s birthrate has been low since the 1970s, and a new generation of babies wouldn’t be paying into the system for around 18 years, which would be after the surplus has been exhausted. This means the only way to increase the population fast enough is through immigration. Given the current government’s anti-immigration stance, this is a very unlikely path.

Conclusion

Social Security does not add to the national debt. The government has not raided its coffers. Its funds are not tossed into a general funding bucket. But it faces a looming shortfall that will significantly reduce benefits if no action is taken.

Receipts: Higher Minimum Wages Do Not Cause Job Loss or High Prices

The federal minimum wage is a poverty wage in every state in the nation, and half of all full-time workers do not earn a livable wage. There is a simple solution to this problem. Raise the federal minimum wage to a livable wage. But whenever this is discussed, there is always an army of propagandists comprised of corporate lobbyists, industry groups, po…