Why Gas Prices Matter

Gas prices change quickly, but their economic impact builds more slowly.

Prices have risen sharply in recent weeks following the conflict with Iran. Regular gas is approaching $4 a gallon nationwide, while diesel is already above $5.

If you drive about an hour each day, you’ll spend roughly $3,000 a year on gas at $4 a gallon. That’s an increase of almost $1,000 compared to before the recent spike. It may not seem like a crisis on its own, but gas is an unavoidable necessity that is deeply tied to the rest of the economy.

Let’s start with the basics.

Financial experts generally recommend keeping total transportation costs between 10–15% of take-home pay. That includes gas, insurance, loan payments, maintenance, and repairs.

The median personal income is around $45,000. At $3,000 a year, gas alone can approach 10% of take-home pay for many households. At the same time, automotive maintenance and repair costs have been rising faster than wages in recent years, putting additional pressure on already tight budgets.

The burden is not evenly distributed. Roughly half of all workers fall below the median income, and those who live in suburban and rural areas often drive longer distances and have fewer transportation options, so higher gas prices take up a larger share of their income.

Unlike many other expenses, fuel costs are difficult to reduce in the short term. Most people can’t quickly change where they live, how far they commute, or what kind of vehicle they drive.

These rising gas prices are happening at a time when a large share of full-time workers struggle to consistently cover basic costs like housing, food, healthcare, and transportation. The Urban Institute finds that almost half of American households lack enough income to reach long-term financial stability.

We can see this strain in the data.

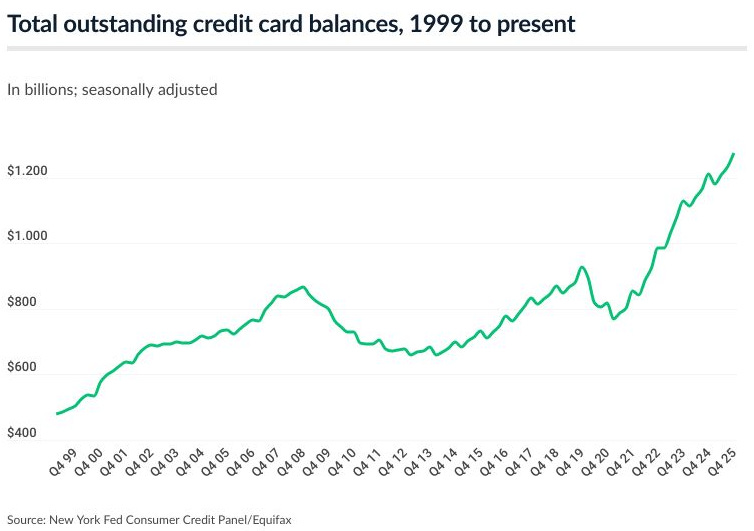

Total outstanding credit card debt has continued to rise since the pandemic, reaching a record $1.28 trillion at the end of 2025. Personal savings rates have fallen from 7.5% in 2019 to around 3.5% today. Hardship withdrawals from retirement accounts have also reached record highs, 3x higher than pre-pandemic levels.

The Federal Reserve has found that a large share of Americans would struggle to cover a $400 emergency expense, meaning that the only way to afford an additional $1,000 in gas costs is to take on more debt or draw more from savings and retirement accounts.

That is the direct impact of higher gas prices. The indirect effects are even broader as higher fuel costs raise the price of nearly everything.

Raw materials have to be transported to factories. Finished goods move from warehouses to stores, then to consumers. Each step depends on transportation, much of it powered by diesel.

When fuel costs rise, those increases compound across the supply chain. Even products that don’t rely directly on oil become more expensive as transportation costs feed into final prices.

And the timing adds additional pressure.

Wholesale inflation data for last month came in higher than expected. These costs often show up in consumer prices in the months that follow, and those figures were measured before the recent increase in fuel prices.

These higher prices haven’t been felt by consumers yet, but they will be soon enough, and that will impact the broader economy.

The United States is largely a consumer-driven economy, relying on consistent spending to sustain growth. As essential costs like gas rise, households adjust by cutting back elsewhere.

Consumer sentiment is already low, lower than during the pandemic, with many expecting economic conditions to worsen throughout the year. That expectation alone can slow spending.

The economy has become increasingly uneven. Higher-income households account for a growing share of total consumer spending, while many lower- and middle-income households face tighter financial constraints. That imbalance can become more pronounced when costs rise, forcing those with less flexibility to pull back their spending more quickly.

How much does a $1 increase in the price of gas matter?

In a strong economy with broad income growth and financial stability, the impact is manageable. But in an economy where many households are already stretched, savings are limited, and spending is increasingly concentrated among a select few, the effects will be significant.

Rising gas prices don’t just increase one expense. They expose the struggles of millions of Americans and how sensitive the broader economy has become to even modest increases in everyday costs.

https://www.lendingtree.com/credit-cards/study/credit-card-debt-statistics/

The 2025 Economic Slowdown

The final numbers of 2025 have arrived, and they are not good. Last year saw a significant economic slowdown, affecting jobs, GDP growth, savings, the deficit, and the lives of millions of hard-working Americans.