Receipts: The Rich Do Not Pay Their Fair Share

Receipts are longer documents that provide concrete information to correct misinformation. These can be bookmarked for easy access to information and to provide accurate talking points, along with graphs, data, and links.

The Claim

We often hear that the rich already pay more than their fair share of taxes. This claim is used to argue that wealthy people deserve more tax cuts or that raising taxes on the rich would be unfair.

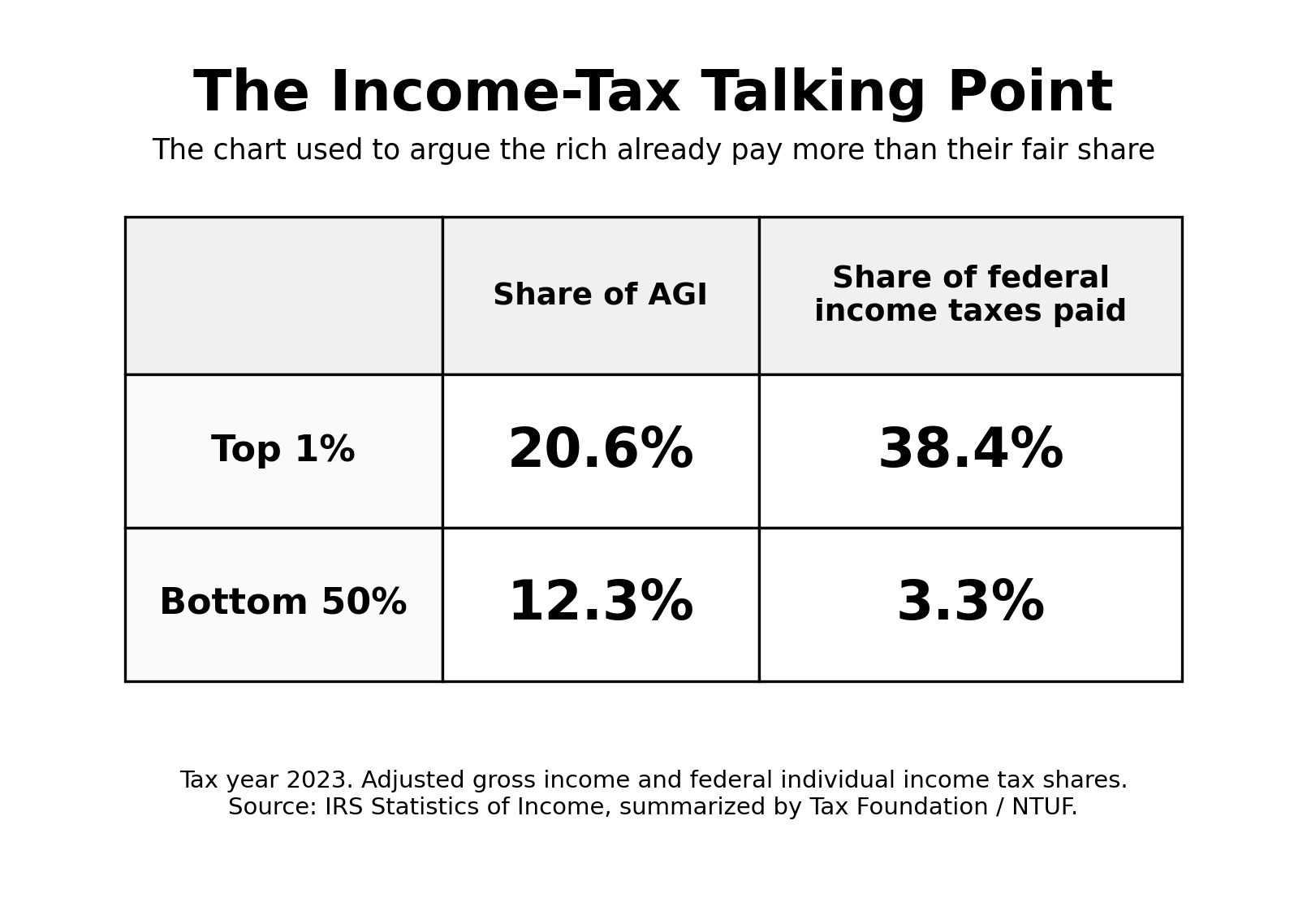

If you challenge that idea, someone may pull out a chart like this:

At first glance, that sounds convincing.

The top 1% received 20.6% of adjusted gross income and paid 38.4% of federal income taxes. The bottom half received 12.3% of adjusted gross income and paid 3.3% of federal income taxes. So the rich must be overtaxed, right?

No.

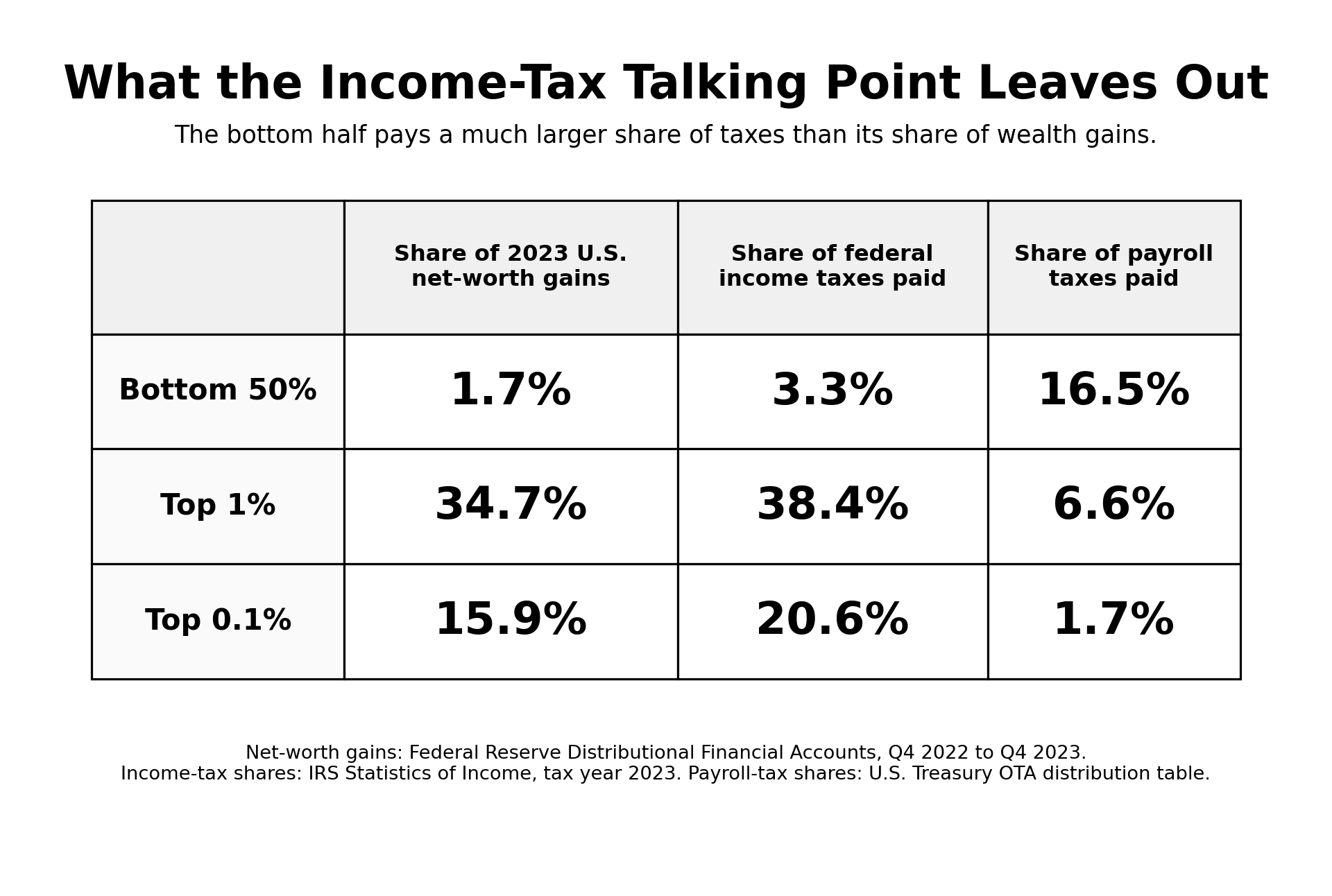

The chart only looks at federal income taxes. It does not include payroll taxes, which are deducted from all workers’ paychecks. And it uses adjusted gross income, which excludes much of the wealth gains that make the richest households richer. It ignores the fact that America taxes work more than wealth.

Sources for this section

Tax Foundation summary of IRS tax year 2023 data: Reports that the top 1% had 20.6% of adjusted gross income and paid 38.4% of federal income taxes, while the bottom 50% had 12.3% of AGI and paid 3.3% of federal income taxes.

NTUF summary of IRS tax year 2023 data: Also summarizes the 2023 IRS percentile data and gives the top 1% threshold and tax shares.

The Reality

The first warning sign that a major part of the situation is being left out of the “rich pay more than their fair share” argument is that it starts with adjusted gross income and addresses only federal income taxes.

When we compare income taxes and payroll taxes to net-worth gains, the picture changes dramatically.

The bottom half of Americans received just 1.7% of the country’s household net-worth gains in 2023, but paid 3.3% of federal income taxes and about 16.5% of federal payroll taxes.

The top 1% captured 34.7% of household net-worth gains and paid 38.4% of federal income taxes, but only about 6.6% of payroll taxes.

There is a group paying more than its fair share, but it isn’t the wealthy. It is the lowest earners. That is because America prefers to tax work rather than money.

Sources for this section

Federal Reserve Distributional Financial Accounts: The Fed’s DFA data provides quarterly household wealth by percentile group, including the top 0.1%, the rest of the top 1%, the next 9%, the next 40%, and the bottom half. The Fed describes this as a comprehensive measure of U.S. household wealth by group.

FRED series for top 1% net worth: FRED lists quarterly net worth held by the top 1% in millions of dollars, sourced from the Federal Reserve’s Distributional Financial Accounts.

FRED series for bottom 50% net worth: FRED lists quarterly net worth held by the bottom 50%, also sourced from the Federal Reserve’s Distributional Financial Accounts.

Treasury Office of Tax Analysis distribution table: Treasury’s 2024 current-law distribution table breaks federal tax burden into categories, including individual income taxes and payroll taxes by income group. The payroll-tax shares above are calculated from that table.

When Wealth Is Not Income

Most working-class income comes from getting paid for doing labor. The government is great at taxing paychecks. Your employer reports your wages. Federal income taxes are withheld. Social Security and Medicare taxes come out automatically. At the end of the year, you file taxes to compare what was withheld with what you actually owed.

Wealth works differently.

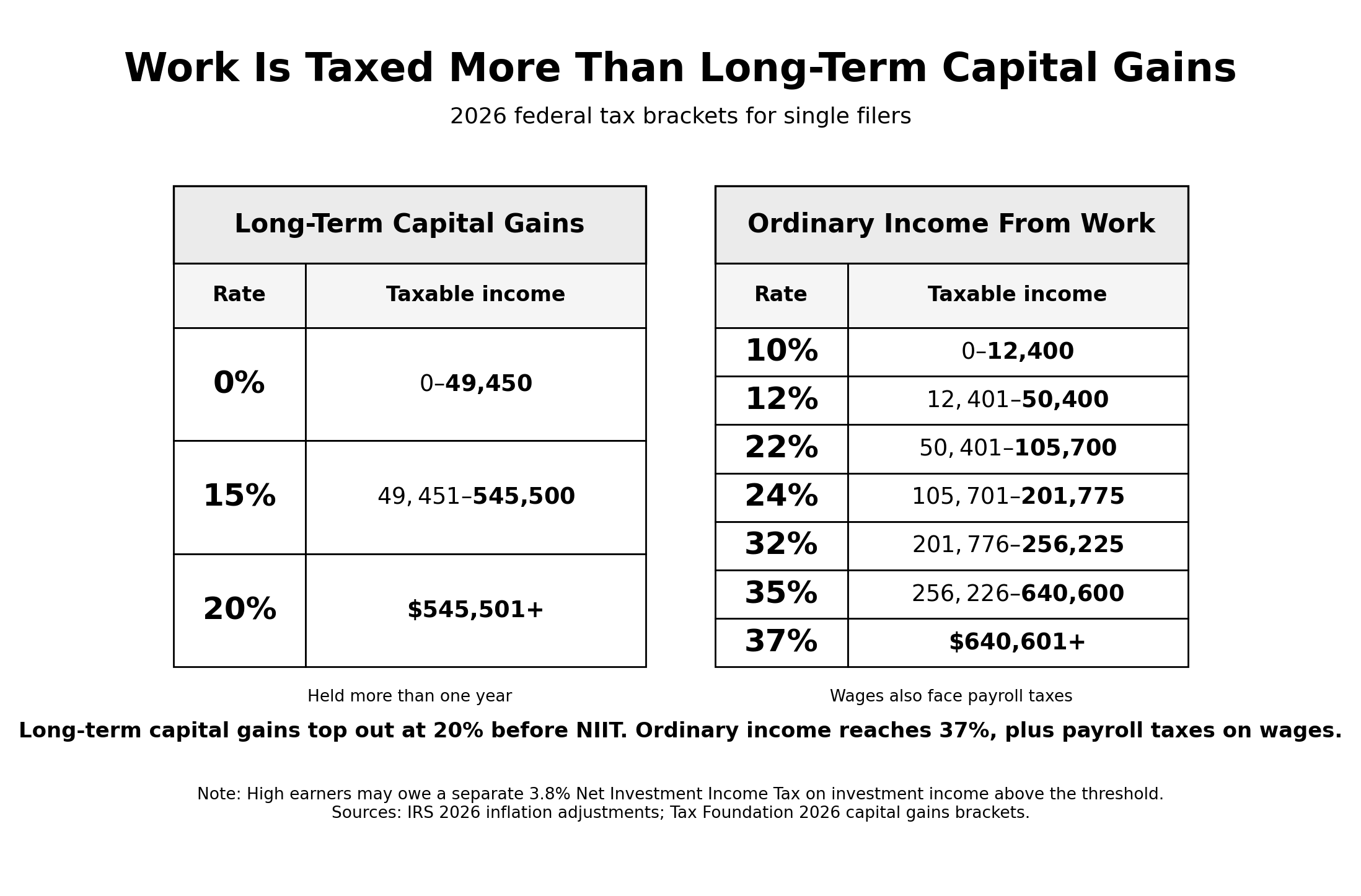

A large share of wealthy income comes from investments. If you buy stock for $1,000 and later sell it for $10,000, the $9,000 gain is a capital gain. If you sell the investment after holding it for one year or less, it is a short-term capital gain and is generally taxed like ordinary income. But if you sell the investment after holding it for more than a year, it is a long-term capital gain and is taxed at lower rates.

High earners may also owe the Net Investment Income Tax, or NIIT. NIIT is a separate 3.8% tax on certain investment income for people above the income threshold. For single filers, the threshold is $200,000.

So the top federal rate on long-term capital gains is generally 23.8% when NIIT applies. Now compare that to income from work.

Ordinary income tax rates go up to 37%, and wages are also subject to payroll taxes. There is no special 0% tax bracket for wages, the way there is for long-term capital gains. And by the time a single filer’s ordinary taxable income exceeds $50,000, it has reached a 22% tax bracket. Quite a bit higher than how large wealth gains are taxed.

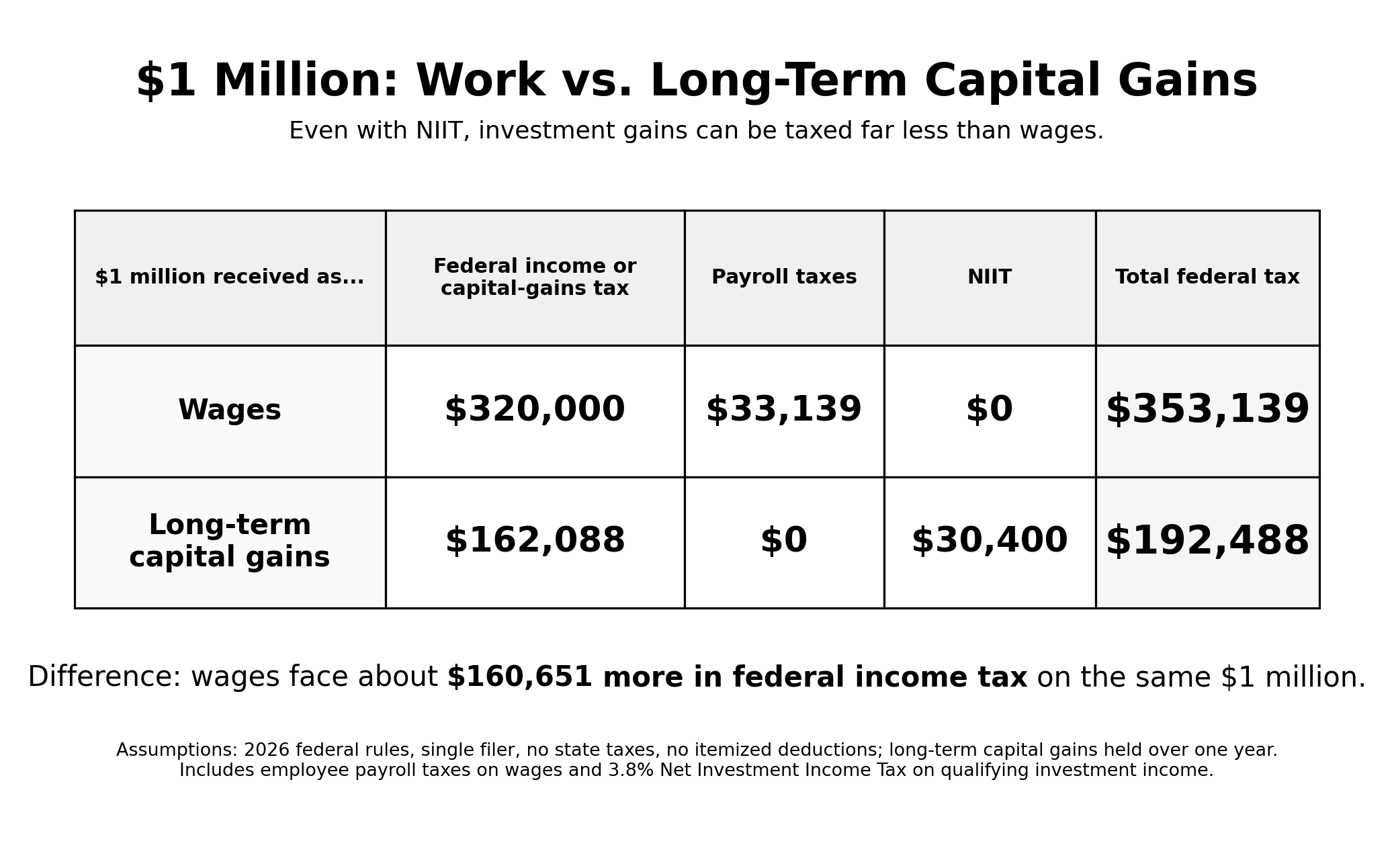

Even for the rich, the tax code does not treat work and wealth the same. Here is a simple example.

Assume a single filer receives $1,000,000 in wages. Now compare that with someone who receives $1,000,000 in long-term capital gains. Using 2026 federal brackets, the standard deduction, no state taxes, and including NIIT where it applies:

Even after including NIIT, $1 million in long-term capital gains can face about $160,000 less in federal tax than $1 million in wages.

If a stock or other asset rises in value but the owner does not sell it, the gain is unrealized. Unrealized gains are not taxed. This makes sense. The owner hasn’t yet received the money from the gains, and the value could rise or fall before they sell it.

Much of the wealth gains of the highest earners are in unrealized capital gains. But they have a trick for using and benefiting from those gains without paying taxes.

Wealthy people can take out a loan against the value of their unrealized capital gains and use that loan to pay their bills, buy things, or even invest further to increase their wealth, without ever paying any income tax. One reason this is worth it is that the interest on the loans is much lower than the tax rate that would be paid on the capital gains.

Even more incredible is that if the loan is used on another investment, the interest for the loan can be deducted from investment income, further reducing their tax burden. And this is exactly what many wealthy people do. Below are some links to great descriptions of this practice, which has sometimes been labeled as “Buy, Borrow, Die”.

We discussed the “Buy” and “Borrow” parts of that strategy. The “Die” part matters too.

When someone dies and passes an appreciated asset to heirs, the asset often receives a stepped-up basis. That means the tax basis is reset to the value at the time of inheritance.

Example:

Someone buys stock for $1,000.

They hold it until death, when it is worth $40,000.

Their heir receives it with a stepped-up basis of $40,000.

If the heir sells it immediately for $40,000, the $39,000 gain is not taxed as capital gains income.

That means the wealthy can grow their wealth, borrow against it, transfer to heirs, and avoid income tax on any of it.

Work is taxed now. Wealth can often be taxed later, taxed less, or sometimes not taxed as income at all.

Sources for this section

IRS Topic 559: Explains the 3.8% Net Investment Income Tax and the income thresholds, including $200,000 for single filers.

IRS 2026 inflation adjustments: Lists 2026 ordinary income tax brackets and the $16,100 standard deduction for single filers.

2026 capital gains tax brackets: Kiplinger’s 2026 capital-gains tax guide lists the long-term capital gains thresholds, including 0% up to $49,450 for single filers and 20% beginning above $545,500.

When Income Is Hidden

The rich have numerous ways to hide their income to avoid paying taxes. Everything from loopholes, loans, deductions, charities, and offshore accounts.

There is the yacht deduction. The way this works is that someone can buy a nice, expensive yacht and, as long as they then charter it out to profit from it, they can deduct the entire cost of the yacht from their income the same year they buy it. So when a rich person does this and buys a $5 million yacht, their income is treated as $5 million lower than what it actually is.

Then there are huge charitable donations, which sound like a good thing, and can be, but some are simply shady ways to protect wealth.

Billionaire Charles Johnson donated a mansion to his own private foundation to gain $38 million in tax savings. The agreement was supposed to be that in exchange for these tax breaks, the mansion would be open to the public 40 hours each week. Instead, a few dozen lottery winners were allowed a 2-hour tour on Wednesday each week. It was not actually a gift to the public. It was just a tax haven often used for other, non-public events.

Over $1 trillion worth of real estate, artwork, stocks, and other assets are held in these charitable trusts. But many are not truly charitable.

There is a ProPublica article that discusses these foundations and includes a bit on Ken Xie, who had received $30 million in tax breaks from his charitable foundation. This foundation bought a $3 million home from his girlfriend and then allowed her to continue living there. Xie lived there part of the time, too.

The Trump Foundation was shut down for misconduct, and Donald Trump was forced to pay $2 million. Sometimes the abuse of the system is caught, but even then, prosecution can be lengthy, complicated, and expensive.

There are offshore trusts and shell companies used to hide income, some of it legal, some of it not. I talked about the yacht deduction. There are other clever ways to convert personal expenses, such as jets and cars, into business expenses through passthrough LLCs.

The wealthy hide their money, reclassify income, and do everything they can to avoid taxes. So whenever someone claims that the wealthy are paying more than their fair share, know that they’re hiding large portions of their share altogether.

Sources for this section

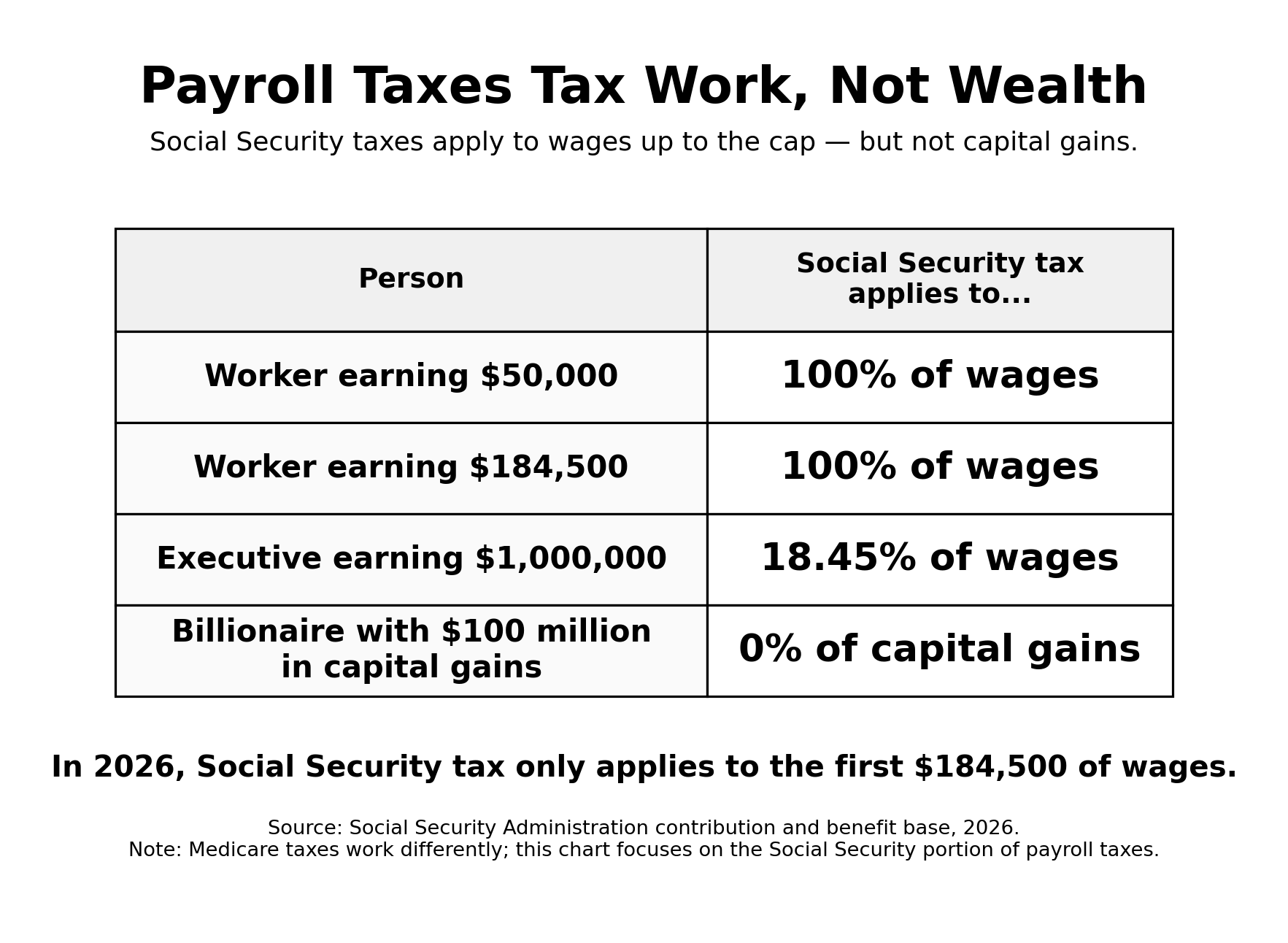

Payroll Taxes Expose The Trick

Those who claim the rich pay more than their fair share intentionally leave out payroll taxes because it exposes how the tax burden is actually greatest on the lowest earners.

Payroll taxes are the taxes workers see every paycheck. They fund Social Security and Medicare. For many low- and middle-income workers, payroll taxes are one of the biggest federal taxes they pay.

The bottom half of Americans paid about 16.5% of federal payroll taxes, according to the Treasury’s distribution data. The top 1% paid about 6.6%. That is a very different picture from the income-tax chart. There are two major reasons. First, Social Security taxes are capped. In 2026, only the first $184,500 of wages are subject to Social Security tax.

Second, payroll taxes apply to work, not wealth.

Capital gains are not subject to Social Security payroll taxes. Unrealized gains are not. Loans against assets are not.

Medicare is different from Social Security because its tax cap was removed in 1993. High-wage workers also pay an additional Medicare tax above the income threshold. But Medicare payroll taxes still mainly apply to wages and self-employment income. They do not apply to capital gains.

There’s another trick the wealthy use to avoid Medicare taxes: exploiting a well-known loophole that has been abused for decades, one that Congress has backed down from fixing under pressure from the rich.

By creating a limited partnership through which money can be funneled, self-employment tax can be avoided through a loophole created while trying to stop the abuse of Social Security by government employees.

This loophole wasn’t used much until the tax cap on Medicare was removed, at which point the rich began looking for a way to avoid the larger tax. This article by ProPublica discusses the full scheme and even highlights a case where a person could form a limited partnership himself, with each partner being a different business he owned.

These are the lengths the wealthy go to in order to avoid paying their taxes.

Sources for this section

ProPublica Medicare tax loophole: exposes limited partnership schemes to avoid paying Medicare taxes.

SSA contribution and benefit base: The Social Security taxable maximum is $184,500 in 2026, and the OASDI tax rate is 6.2% for employees and 6.2% for employers.

IRS NIIT explanation: NIIT is a 3.8% tax on certain net investment income above the income threshold, not a standard payroll tax on all wealth gains.

Treasury distribution table: Used to calculate payroll-tax shares by income group.

Low Earners Are Not The Freeloaders

It is true that 31% of income tax filers do not pay any federal income tax, but this isn’t because they’re freeloading off the system. It is because they don’t have any money to give.

Just like how businesses only pay income tax on profits, not money that was used to operate the business, people get to exempt a certain amount of their income from federal income tax needed to live. We’ve acknowledged that it costs a certain amount of money simply to exist, so the government doesn’t tax you on that small amount.

These people struggling to exist, still pay payroll taxes, so it is wrong to claim they don’t pay taxes. There are also sales tax, state and local taxes, and tariffs, which are taxes. To suggest that someone who is being taxed in so many ways is a freeloader is shameful slander.

But what do you call it when the richest 25 Americans see their wealth increase over 4 years by over $400 billion but pay only $13.6 billion in income taxes, a 3.4% rate? Or when someone who increases their net worth by amost $4 billion in a year ends up paying zero federal income tax?

That’s what ProPublica found when looking through tax records of the wealthiest Americans, linked below.

One of the more shocking discoveries was that Jeff Bezos not only paid zero federal income tax in 2011, but he also claimed and received a $4,000 child tax credit while his net worth was around $18 billion. The government giving a billionaire money? Who is the freeloader?

America has a progressive income tax. Someone making billions isn’t supposed to be paying a lower rate than a teacher, firefighter, plumber, or any other hard-working American. The wealthy aren’t paying the proper tax rate because a lot of their wealth isn’t even being taxed.

Sources for this section

ProPublica overview: Explains how billionaires can pay little or sometimes nothing in federal income taxes compared with their wealth growth.

ProPublica IRS Files: ProPublica reported that the 25 wealthiest Americans saw their wealth rise by $401 billion from 2014 to 2018 while paying $13.6 billion in federal income taxes, which ProPublica calculated as a 3.4% “true tax rate” relative to wealth gains.

Pay Workers More

There is one obvious answer to the complaint that low earners do not pay enough federal income tax:

Pay workers more.

If workers earned more, more of them would owe federal income tax, and fewer would need help for federal assistance. Higher wages increase tax revenue, reduce pressure on safety-net programs, and boost the economy through consumer spending.

The problem is not that low-income workers are undertaxed. The problem is that too many workers are underpaid. The 2026 Dayforce/Living Wage Institute report found that half of full-time U.S. workers do not earn a livable wage. An increase of 5% since 2021. So when someone says low earners should pay more income tax, the answer is simple:

Pay them more.

Sources for this section

Dayforce/Living Wage Institute: study on how many workers are paid livable wages.

The Stock Market Belongs Mostly To The Rich

Like trickle-down economics, the claims that lower tax rates on investments held over one year (long-term capital gains) increase corporate investment and economic growth turned out to be false. And, like trickle-down economics, the policy mainly benefits the rich.

The top 1% own half of the wealth invested in stocks and mutual funds, the bottom 50% just 1%. In plain language: the top 1% owns about half of the money Americans have invested in the markets, while the bottom half owns almost none of it.

Lower tax rates on long-term capital gains allow the rich to pay lower taxes.

Sources for this section

FRED/Federal Reserve corporate equities and mutual fund shares: FRED provides the Federal Reserve DFA data series for corporate equities and mutual fund shares by wealth group, including the bottom 50%, top 1%, and top 0.1%.

Federal Reserve DFA overview: Explains that the dataset breaks household wealth into percentile groups and includes wealth composition.

How To Fix It

The rich are not paying more than their fair share. They’re not even paying their share because large portions of their income are taxed at a lower rate, and much of their wealth gains are not taxed at all.

To fix that, we need to tax all money fairly, not tax work more than wealth.

1. Tax capital gains like income

Long-term capital gains and qualified dividends should be taxed at ordinary income tax rates for high-income households.

2. End stepped-up basis

Capital gains should not disappear at death.

If wealthy people can hold assets until death and pass them to heirs with the gains erased for income-tax purposes, then the capital-gains tax becomes optional for generational wealth.

End stepped-up basis, or tax large unrealized gains at death.

3. Limit buy-borrow-die

Ultra-wealthy households should not be able to live off loans against appreciated assets forever while avoiding capital-gains taxes.

Borrowing against large appreciated assets should be treated as a taxable event.

4. Make payroll taxes fairer

Lift or eliminate the Social Security wage cap.

Right now, a worker making $60,000 pays Social Security tax on every dollar of wages, while someone making $1 million in wages stops paying Social Security tax after the first $184,500.

5. Apply Medicare taxes more consistently

High-income business and investment income should not be able to slip around Medicare taxes through clever structures.

If ordinary workers cannot opt out of Medicare taxes, wealthy business owners and financiers should not be able to either.

6. Fund enforcement

A tax system that lets the rich use complex structures requires an IRS capable of auditing them.

Defunding tax enforcement is effectively a tax cut for people wealthy enough to hide behind complexity.